Quick Answer: Afterpay typically does not report regular on-time payments to major credit bureaus like Experian, Equifax, or TransUnion. So, using Afterpay and paying on time may not help you build credit. But unpaid balances can still become a credit problem if they are sent to collections.

Afterpay feels a lot like credit. You buy something now, split the cost into smaller payments, and pay it back over time. So it makes sense to ask whether Afterpay reports your payments to credit bureaus.

If you’re also wondering whether Afterpay can change your credit score, read our full guide on does Afterpay affect your credit.

The answer is a little different from how credit cards and loans work. With a credit card, your payment history and balance are usually reported to the major credit bureaus. With Afterpay, normal payment activity is usually handled inside the Afterpay system instead.

That’s good in one way. Your regular Afterpay use may not show up on your credit report. But it also means paying on time may not help your credit score grow. And if you stop paying, the story can change fast.

Does Afterpay Report Regular Payments to Credit Bureaus?

In most cases, Afterpay does not report your regular on-time payments to credit bureaus. That means your normal Afterpay purchases may not appear on your credit report the way a credit card, auto loan, student loan, or personal loan might.

This is important because many people think every payment plan helps build credit. It doesn’t always work like that. If a company does not report your payment history to Experian, Equifax, or TransUnion, then those on-time payments usually won’t be added to your credit file.

So if you pay Afterpay on time, that’s still a good thing. It keeps your account in good shape. It helps you avoid late fees. It may also protect your spending limit with Afterpay. But it may not raise your credit score.

A simple way to think about it is this: Afterpay can help you split a purchase, but it’s not usually a credit-building tool.

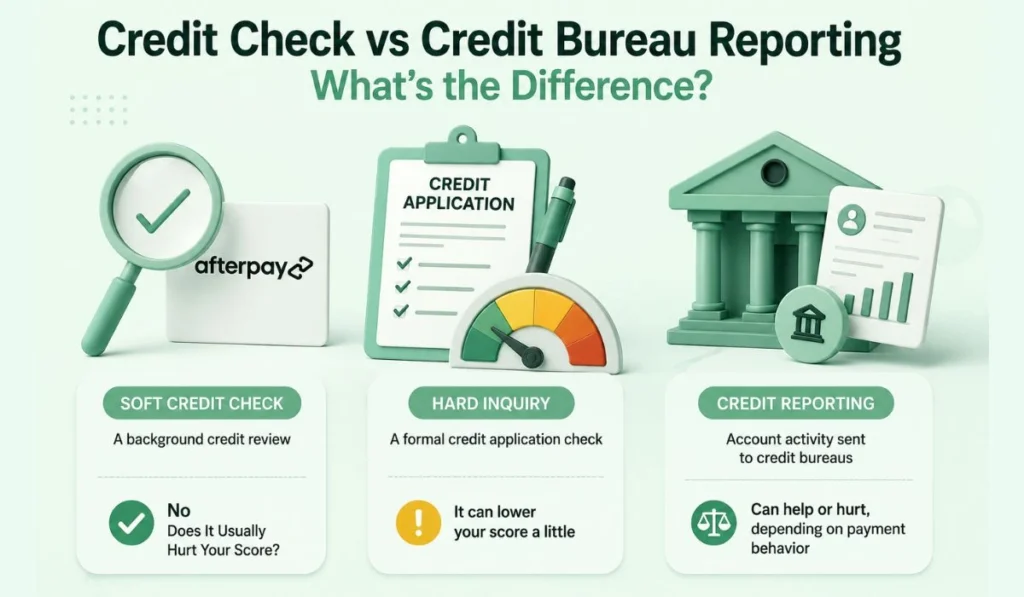

Credit Check vs Credit Bureau Reporting: What’s the Difference?

This part confuses a lot of people, and fair enough. A credit check and credit reporting sound similar, but they are not the same thing.

Afterpay may use a soft credit check when you sign up or when it reviews your account. A soft check is just a quick look at some credit-related information. It does not lower your credit score, and it does not show up to lenders like a hard inquiry.

A hard credit inquiry is different. That usually happens when you apply for a credit card, mortgage, car loan, or personal loan. A hard inquiry can lower your score a little for a short time.

Credit bureau reporting is another thing again. That means a company sends your account activity, like payments and balances, to credit bureaus.

| Term | What It Means | Does It Usually Hurt Your Score? |

|---|---|---|

| Soft credit check | A background credit review | No |

| Hard inquiry | A formal credit application check | It can lower your score a little |

| Credit reporting | Account activity sent to credit bureaus | Can help or hurt, depending on payment behavior |

So, even if Afterpay checks some information, that does not always mean it reports your payment history to the credit bureaus.

When Afterpay Could Still Show Up on Your Credit Report

This is the serious part. Afterpay may not report normal payments, but unpaid debt can still create credit damage.

If you miss a payment, Afterpay may charge a late fee, pause your account, or lower your ability to make new purchases. That alone may not always show up on your credit report right away.

But if you leave the balance unpaid for too long, the account may be sent to a third-party debt collector. Once collections are involved, things can get much worse. A collection account may appear on your credit report, and that can hurt your credit score.

This is the one way Afterpay can turn into a real credit problem. Not because you used it once. Not because you split a purchase into smaller payments. The danger comes when a small unpaid balance becomes a collections account.

And yes, even a small debt can be annoying later. A missed Afterpay payment for a pair of shoes or a small online order may not feel serious at first. But if it sits unpaid and gets passed to collections, it can create a much bigger headache than the purchase was worth.

How Different Afterpay Situations May Affect Credit Reporting

Here’s a simple breakdown.

| Afterpay Situation | Likely Credit Bureau Impact | What It Means |

|---|---|---|

| You pay on time | Usually not reported | May not help or hurt your credit score |

| You miss one payment but fix it fast | May not show on credit report | You may face a fee or account limit |

| You miss several payments | Risk increases | Afterpay may pause your account or keep trying to collect |

| Debt goes to collections | Could show on credit report | This can hurt your credit score |

| You apply for a loan while using BNPL | May affect lender review | Lenders may count BNPL payments as monthly obligations |

The last point is worth keeping in mind. In 2026, many lenders look beyond just your credit score. If you apply for a home loan, car loan, or personal loan, they may review your bank statements too.

If they see regular Afterpay payments, they may treat them as part of your monthly obligations. That does not mean you will be rejected. But it can affect how affordable your loan looks on paper.

How to Use Afterpay Without Credit Report Problems

The safest way to use Afterpay is to treat it like real debt. Not free money. Not a discount. Just a short payment plan.

Only use it for purchases you already know you can afford. If the full price would break your budget, splitting it into smaller payments may only delay the stress.

I also recommend linking Afterpay to a debit card instead of a credit card. Why? Because using a credit card to pay for a buy now, pay later service is debt on top of debt. It can get messy. A debit card keeps it closer to the money you already have in your bank account.

Set reminders before each due date. Don’t trust memory too much here. A simple phone alert can help you avoid late fees, failed payments, and account restrictions.

Try not to open too many BNPL plans at the same time. One small payment plan may be easy. Four or five active plans can sneak up on you, especially when they all hit in the same week.

It’s also smart to check your credit report once in a while. Afterpay may not appear there during normal use, but you still want to catch any collection account, mistake, or unknown item early.

FAQs About Afterpay and Credit Bureau Reporting

Does Afterpay report to Experian?

Afterpay typically does not report regular on-time payments to Experian. But if an unpaid balance goes to collections, that collection account may be reported depending on how the debt is handled.

Does Afterpay report to Equifax or TransUnion?

Afterpay typically does not report regular on-time payments to Experian. But if an unpaid balance goes to collections, that collection account may be reported depending on how the debt is handled.

Does Afterpay report late payments?

Afterpay may not report a simple late payment directly in many cases. But late payments can still lead to fees, account limits, and collection risk if the balance stays unpaid.

Can Afterpay help build credit?

Usually, Afterpay is not a strong credit-building tool. If on-time payments are not reported to the credit bureaus, they usually won’t help build your credit history.

Does Afterpay show up on a credit report?

Regular Afterpay use may not show up on your credit report. But a collection account related to unpaid Afterpay debt could appear and hurt your score.

Final Thoughts

Afterpay usually does not report regular payments to credit bureaus, so normal use may not help or hurt your credit score. The real risk starts when payments are missed and the debt stays unpaid. Keep it simple: only buy what you can afford, pay on time, and don’t let a small balance turn into a collections problem.