Quick Answer: Afterpay is a buy now, pay later service that lets shoppers split eligible purchases into smaller payments. Many people use it at checkout online or in stores. The common Pay in 4 option lets you pay over time instead of paying the full amount upfront.

You may have seen Afterpay while shopping online and wondered what it really means. It sounds simple at first: buy something now and pay for it later. But before using it, it helps to understand how the payments work, what happens at checkout, and what you’re agreeing to.

Afterpay can be useful for splitting an eligible purchase into smaller payments, but it still comes with due dates, account terms, and possible fees if the payments are missed. This guide explains what Afterpay is, how it works, and what to know before using it.

What Is Afterpay?

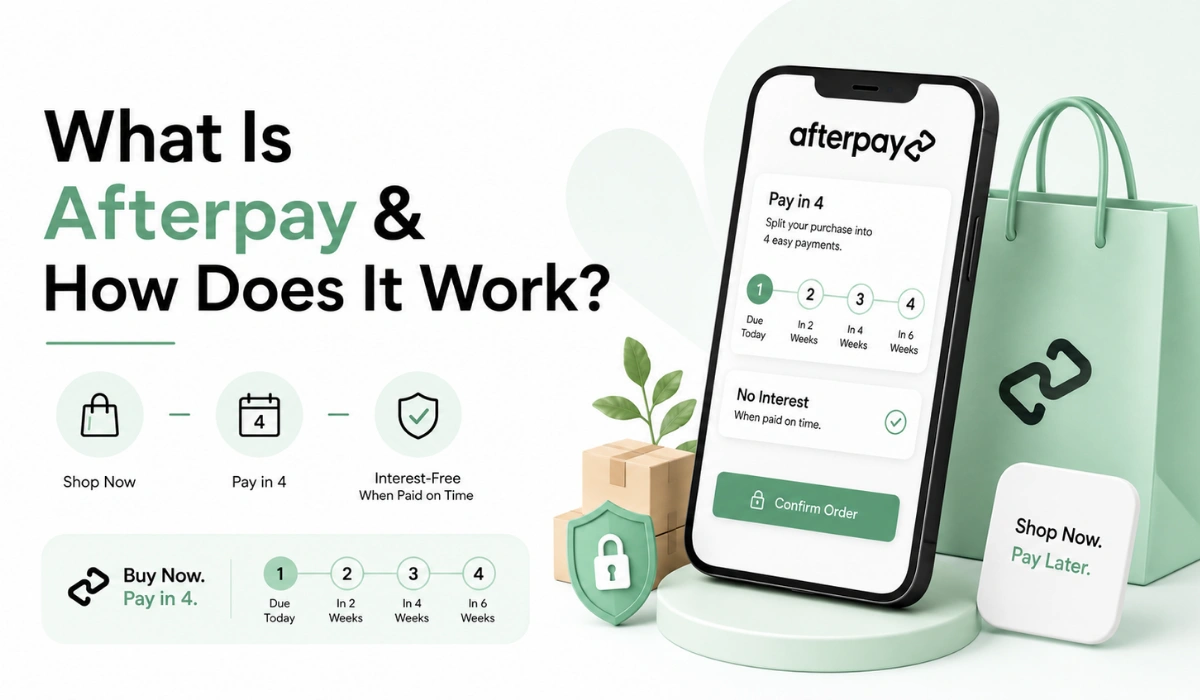

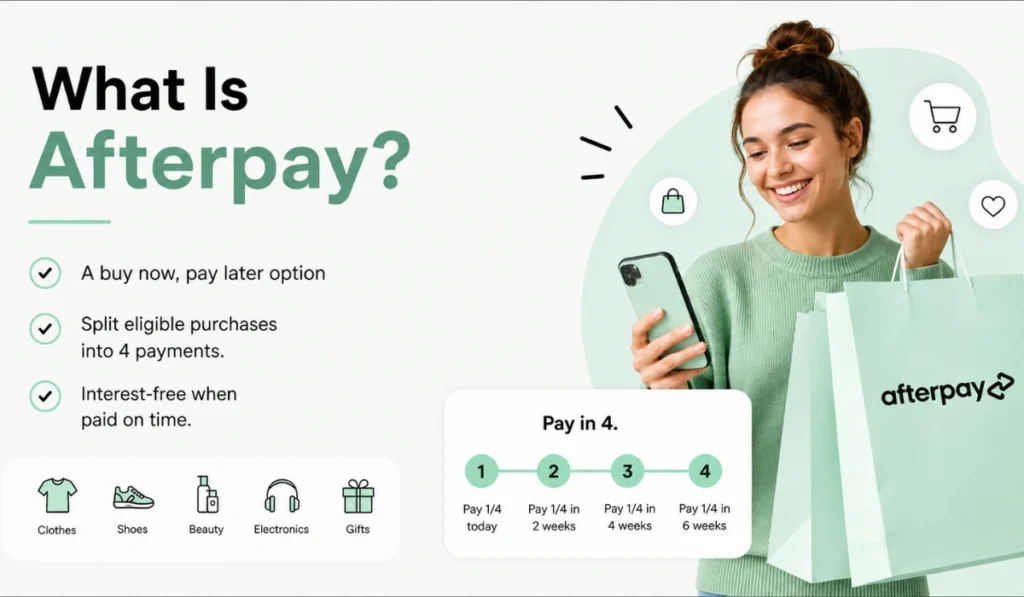

Afterpay is a payment method that you might see when shopping online or in a store. The eligible purchases could be divided by the smaller scheduled payments instead of paying the total price at once. It is commonly referred to as buy now, pay later (BNPL).

One easy manner of thinking about it is the following: purchase it now, then pay it in instalment. The order is still processed at the store, however, the payment plan between you and Afterpay is handled by Afterpay.

The most prevalent one is Pay in 4. That implies that the purchase will be divided into four payments with a short time frame. Afterpay claims its Pay in 4 feature is no-interest at partnering brands when the payments are made on time.

This is what makes people use Afterpay to purchase clothes, shoes, beauty products, electronics and gifts, along with other daily purchases. It may make purchase easier to manage, yet, it must be repaid at the appropriate time.

How Does Afterpay Work?

Afterpay works at checkout. You shop like normal, choose Afterpay as the payment method if it is available, then follow the steps to complete the order. First-time users may need to create an account or complete a quick sign-up process. Returning users may only need to log in through the official Afterpay flow.

Once the purchase is approved, Afterpay splits the total into scheduled payments. Usually, the first payment is due at checkout or around the time of purchase. The rest are charged later based on the payment schedule shown in your account.

Here is the basic flow:

- Shop at a store that offers Afterpay

You choose items from a participating store online or in person. - Select Afterpay at checkout

If the store supports it, Afterpay may appear as a payment option. - Review the payment schedule

You should see how much is due now and when the later payments are due. - Complete the purchase

If approved, the store processes the order and Afterpay manages the payment plan. - Pay the remaining installments

Payments are usually charged automatically to the payment method on file.

This matters because Afterpay is not free money. It can spread out the cost, but the payment dates still matter. Missing them can lead to problems, like late fees or a lower spending limit.

Example of an Afterpay Payment Schedule

Here is a simple example to show how Pay in 4 can look. This is only an example, not a promise of how every purchase will be split.

| Example Purchase | Payment | When It May Be Due |

|---|---|---|

| $100 order | $25 | At checkout |

| $100 order | $25 | Later scheduled date |

| $100 order | $25 | Later scheduled date |

| $100 order | $25 | Final scheduled date |

The real payment dates can depend on your order, your account, and the terms shown at checkout. Always check the schedule before you agree to the purchase. It’s easy to skip over that screen, but that’s the part that tells you what you’re signing up for.

Is Afterpay the Same as a Credit Card?

Afterpay is not the same as a normal credit card. A credit card usually gives you a revolving credit line. You can keep using it up to your limit, then pay the balance over time. Interest may apply if you carry a balance.

Afterpay works more like a short payment plan for a specific purchase. You use it for an eligible order, then pay that order back based on the schedule shown. You may have a spending limit, but that limit can change based on different factors.

Here’s a simple comparison:

| Feature | Afterpay | Credit Card | Debit Card |

|---|---|---|---|

| Payment style | Split into scheduled payments | Pay now or carry balance | Pay from bank balance |

| Interest | Pay in 4 may be interest-free when paid on time at partner merchants | Interest may apply | No credit interest |

| Approval | Checked per account/order | Based on card approval and credit line | Based on available money |

| Best for | Spreading out eligible purchases | Flexible credit use | Paying directly |

This is where it gets tricky. Some people think Afterpay is just like paying with cash later. It’s not. You are still agreeing to a payment schedule, and missed payments can create extra issues.

Who Can Use Afterpay?

Not everyone can use Afterpay. In the United States, Afterpay’s help page says users generally need to be at least 18 years old, live in one of the 50 states or Washington, D.C., and have valid contact and payment details. It also says Afterpay is not available in U.S. territories.

You may also need a valid email address, mobile number, U.S. delivery address, and an accepted payment method. Approval is not always guaranteed. Afterpay can review different details before allowing a purchase.

So if you see Afterpay at checkout, that does not always mean the order will be approved. Your account status, payment history, order amount, and the store may all play a part.

Where Can You Use Afterpay?

You can use Afterpay at participating brands and stores. Some stores offer it online. Some may offer it in store through the Afterpay app or Afterpay Card. Availability can change, so it’s smart to check the store’s checkout page or the Afterpay app before planning around it.

Afterpay says shoppers can use it with many brands and products online and in stores, but that does not mean it works everywhere.

For example, one store may accept Afterpay online but not in store. Another store may show Afterpay for some products but not others. Some carts may not qualify because of the order amount, item type, or checkout rules.

The main thing to remember: look for Afterpay at checkout. If it is not shown there, the store or order may not support it.

Does Afterpay Charge Interest or Fees?

Afterpay Pay in 4 is usually known for interest-free payments when you pay on time at partnered merchants. That is one of the main reasons people use it. But you still need to be careful with fees.

Afterpay’s U.S. help page says Pay in 4 is free when you pay on time for orders made with partnered merchants. It also notes that finance fees may apply in some non-partnered merchant situations inside the app, such as certain Single Use Payment or gift card purchases.

Late fees may apply if a scheduled payment is not paid after the grace period. Afterpay says late fees are capped, and the total late fees on an order will never be more than 25% of the initial order value.

So, no, Afterpay is not always expensive. But it can cost more if payments are missed or if you use a payment type that has extra terms. Always read the payment screen before you confirm.

Is Afterpay Safe to Use?

Afterpay can be safe to use when you use the official app, the official website, or a real store checkout. The bigger risk is usually not the tool itself. The risk is using it without understanding the payment dates, or clicking fake links that pretend to be Afterpay.

A good habit is to manage your account only through official Afterpay channels. Don’t enter account details on random pages. Don’t trust text messages or emails that pressure you to click fast. If something feels off, open the app yourself instead of using the link.

There is also a budget side to safety. Afterpay can make a purchase feel smaller because you only pay part of it upfront. That can be helpful, but it can also make it easier to buy more than planned. Small payments still add up.

Stay safe while using Afterpay by reading our Afterpay Text Scam Guide to avoid falling for fake messages.

Pros and Cons of Afterpay

Afterpay can be useful, but it is not perfect for every shopper. Here’s a plain look at both sides.

| Pros | Cons |

|---|---|

| Splits eligible purchases into smaller payments | Missed payments can lead to late fees |

| Pay in 4 may be interest-free when paid on time | Approval is not guaranteed |

| Can be used at many participating stores | Not accepted everywhere |

| Payment schedule is shown before checkout | Multiple orders can become hard to track |

| App can help manage payments | Spending limits may change |

For some people, Afterpay is helpful for planning a purchase. For others, it can make spending feel too easy. That depends on how you use it.

When Afterpay May Not Be the Best Option

Afterpay may not be a good fit if you are already unsure about making the future payments. It may also be risky if you have several payment plans running at the same time. Four small payments can feel simple, but five different orders can get messy fast.

It may also not be the best choice for impulse buying. If you would not buy the item at full price today, it’s worth pausing before splitting the cost. Not always, but often.

You should also be careful if your income changes from week to week. A payment that feels easy today may feel annoying later when the due date comes around.

FAQs About Afterpay

What is Afterpay used for?

Afterpay is used to split eligible purchases into smaller scheduled payments. People often use it for shopping online or in stores where Afterpay is accepted.

Is Afterpay a loan?

Afterpay is a buy now, pay later payment service. Some Afterpay products may work differently, so users should review the terms shown at checkout before agreeing.

Does Afterpay charge interest?

Afterpay Pay in 4 is generally interest-free when you pay on time at partnered merchants. Fees may apply in some cases, especially if payments are missed.

Can anyone use Afterpay?

No. Users need to meet Afterpay’s eligibility rules, and each purchase may still need approval. Seeing Afterpay at checkout does not guarantee approval.

Does Afterpay affect your credit?

This depends on the product, account activity, and current terms. For a full answer, it is better to read a separate guide about Afterpay and credit reporting.

Can you use Afterpay in stores?

Yes, Afterpay may be available in stores through supported checkout options, but it depends on the store and account eligibility. Check the app or store checkout before relying on it.

Final Thoughts

Afterpay is a buy now, pay later service that helps shoppers split eligible purchases into smaller payments. The basic idea is simple, but the details still matter. You should know the payment schedule, possible fees, store availability, and your own budget before using it.

For beginners, the best way to think about Afterpay is this: it can make checkout more flexible, but it does not remove the cost. You still have to pay the full amount over time.

Have you used Afterpay before, or are you still deciding if it makes sense for your shopping style? Leave a comment and share what you’re trying to understand first.